UnRısk Advance To Go

23. July 2024

Calibration Problems – An Inverse Problems View

23. July 2024

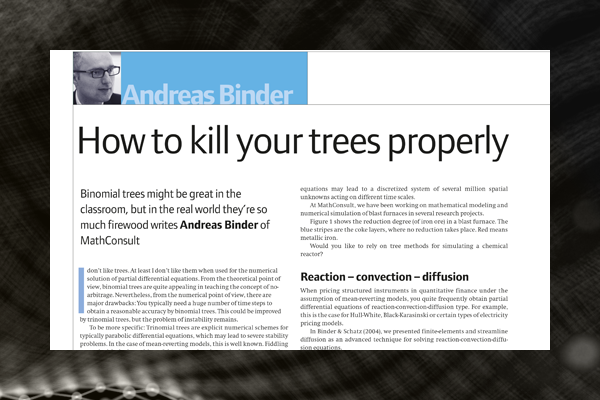

Finite Elements and Streamline Diffusion for the Pricing of Structured Financial Instruments

The document titled "Finite Elements and Streamline Diffusion for the Pricing of Structured Financial Instruments" by Andreas Binder and Andrea Schatz explores advanced numerical techniques for pricing complex financial instruments. The paper focuses on the application of finite element methods (FEM) and streamline diffusion to solve the partial differential equations (PDEs) that arise in financial models, particularly those involving mean-reverting interest rate models like the two-factor Hull-White model.

The authors begin by discussing the limitations of earlier methods such as binomial and trinomial trees and highlight the benefits of FEM in terms of flexibility and accuracy. They delve into the technical aspects of applying FEM to financial models, describing how convection-dominated regions in these models can cause numerical instabilities. To address this, the paper introduces streamline diffusion, a technique that adds artificial diffusion in the direction of the flow, stabilizing the solution and reducing oscillations.

The paper presents detailed mathematical formulations and compares the numerical results obtained using standard FEM, FEM with streamline diffusion, and analytical solutions for pricing zero-coupon bonds with different maturities. The comparison shows that streamline diffusion significantly improves the accuracy and stability of the pricing models, especially for long-term instruments.

In addition to the numerical methods, the authors discuss the software architecture used to implement these techniques, emphasizing the use of object-oriented programming in C++ to create a flexible and scalable framework for financial modeling.